All Categories

Featured

Table of Contents

IUL contracts secure against losses while using some equity risk premium. IRAs and 401(k)s do not use the same downside security, though there is no cap on returns. IULs tend to have have made complex terms and higher charges. High-net-worth people wanting to decrease their tax burden for retirement may profit from spending in an IUL.Some financiers are better off getting term insurance coverage while optimizing their retirement payments, instead of buying IULs.

If the underlying supply market index increases in a given year, owners will see their account rise by a symmetrical amount. Life insurance policy business use a formula for determining just how much to credit your money balance. While that formula is linked to the efficiency of an index, the amount of the credit is usually mosting likely to be much less.

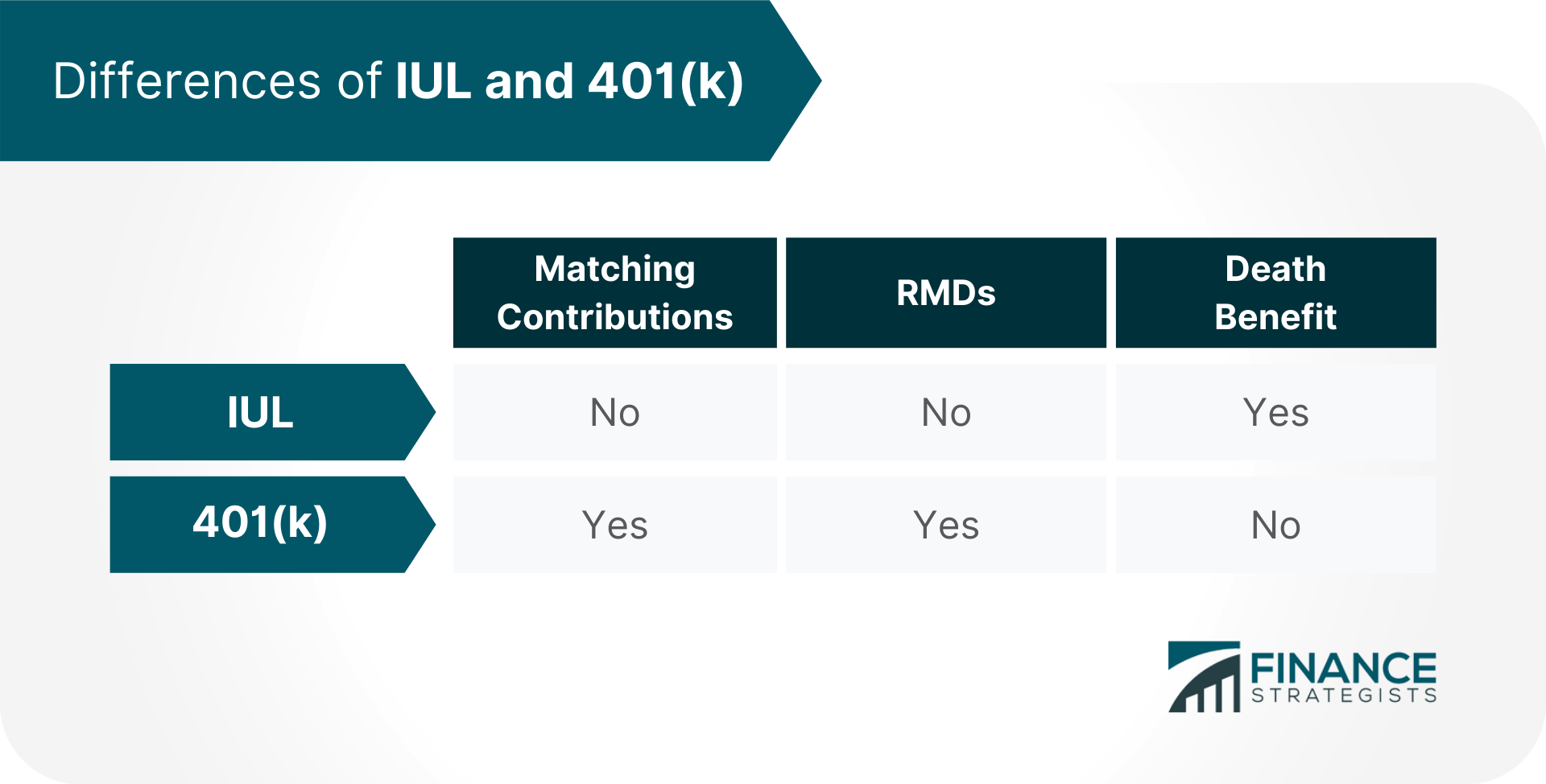

Companies commonly supply coordinating contributions to 401(k)s as an advantage. With an indexed global life policy, there is a cap on the quantity of gains, which can limit your account's growth. These caps have yearly ceilings on account credit scores. So if an index like the S&P 500 increases 12%, your gain might be a portion of that quantity.

What Are The Key Differences Between Iul And 401(k)?

Irreversible life insurance depends on have actually long been a prominent tax obligation sanctuary for such people. If you fall into this category, consider talking with a fee-only economic consultant to talk about whether acquiring permanent insurance policy fits your general approach. For lots of capitalists, though, it may be far better to max out on contributions to tax-advantaged pension, specifically if there are payment matches from a company.

Some plans have an assured rate of return. One of the crucial functions of indexed global life (IUL) is that it provides a tax-free circulations.

Suitable for ages 35-55.: Offers versatile insurance coverage with modest money value in years 15-30. Some things clients ought to consider: In exchange for the death advantage, life insurance items charge costs such as death and expense threat costs and abandonment charges.

Retired life preparation is vital to keeping economic protection and keeping a particular standard of life. of all Americans are fretted about "keeping a comfortable requirement of living in retired life," according to a 2012 survey by Americans for Secure Retirement. Based upon current data, this bulk of Americans are warranted in their issue.

Division of Labor estimates that a person will certainly require to preserve their current requirement of living once they start retirement. Furthermore, one-third of U.S. home owners, in between the ages of 30 and 59, will certainly not be able to maintain their standard of living after retired life, even if they postpone their retirement up until age 70, according to a 2012 research study by the Employee Benefit Research Institute.

Can I Use Iul Instead Of A 401(k) For Retirement?

In the very same year those aged 75 and older held a typical financial obligation of $27,409. Amazingly, that figure had more than increased because 2007 when the typical financial obligation was $13,665, according to the Worker Advantage Research Study Institute (EBRI).

56 percent of American senior citizens still had impressive financial obligations when they retired in 2012, according to a study by CESI Financial obligation Solutions. The Roth IRA and Plan are both tools that can be used to construct significant retirement financial savings.

These financial tools are comparable in that they benefit policyholders who want to create savings at a lower tax obligation price than they may come across in the future. Make each extra attractive for individuals with differing requirements. Identifying which is much better for you depends upon your personal scenario. In either instance, the plan expands based on the passion, or returns, attributed to the account.

That makes Roth IRAs excellent cost savings automobiles for young, lower-income employees that stay in a reduced tax obligation bracket and who will certainly profit from decades of tax-free, compounded development. Because there are no minimum needed payments, a Roth individual retirement account gives financiers control over their personal goals and take the chance of tolerance. Additionally, there are no minimum called for distributions at any kind of age throughout the life of the policy.

a 401k for workers and employers. To contrast ULI and 401K strategies, take a minute to recognize the fundamentals of both products: A 401(k) allows workers make tax-deductible payments and take pleasure in tax-deferred development. Some employers will certainly match component of the employee's payments (iscte iul biblioteca). When employees retire, they usually pay tax obligations on withdrawals as average revenue.

Pros And Cons Of Iul

Like various other long-term life plans, a ULI plan also allots component of the costs to a cash account. Given that these are fixed-index policies, unlike variable life, the policy will likewise have actually a guaranteed minimum, so the money in the money account will certainly not lower if the index decreases.

Plan owners will certainly likewise tax-deferred gains within their cash account. Indexed Universal Life (IUL) vs IRA: A Comparison of Investment Strategies. Check out some highlights of the advantages that global life insurance can offer: Universal life insurance policies don't impose limits on the size of policies, so they may supply a means for staff members to save even more if they have currently maxed out the IRS limits for various other tax-advantaged economic products.

The IUL is far better than a 401(k) or an Individual retirement account when it comes to conserving for retirement. With his almost 50 years of experience as an economic strategist and retirement preparation professional, Doug Andrew can show you precisely why this is the case.

%20Vs.%20Indexed%20Universal%20Life%20(Iul)%20Insurance%3A%20Pros%20And%20Cons){kind=link}

Latest Posts

Universal Life Insurance With Living Benefits

Best Indexed Universal Life Insurance Companies

Is An Iul A Good Investment