All Categories

Featured

Table of Contents

There is no one-size-fits-all when it revives insurance. Obtaining your life insurance policy plan right takes into account a number of elements. [video description: Pleasant music plays as Mark Zagurski speaks to the camera.] In your hectic life, monetary self-reliance can feel like a difficult objective. And retired life might not be leading of mind, because it seems until now away.

Pension, social safety, and whatever they would certainly managed to conserve. It's not that simple today. Fewer companies are offering traditional pension and several business have decreased or terminated their retired life plans and your ability to depend only on social safety and security remains in concern. Also if advantages have not been minimized by the time you retire, social safety alone was never ever intended to be enough to pay for the way of life you desire and deserve.

Now, that might not be you. And it's essential to know that indexed universal life has a whole lot to offer people in their 40s, 50s and older ages, in addition to people who want to retire early. We can craft a solution that fits your details scenario. [video: An illustration of a man appears and his wife and child join them.

This is replaced by an illustration of a document that reads "IUL POLICY - $400,000". The document hovers along a dotted line passing $6,000 increments as it nears an illustrated bubble labeled "age 70".] Currently, mean this 35-year-old guy requires life insurance policy to shield his family members and a means to supplement his retirement earnings. By age 90, he'll have obtained virtually$900,000 in tax-free revenue. [video: Text boxes appear that read "$400,000 or more of protection" and "tax-free income through policy loans and withdrawals".] And needs to he pass away around this moment, he'll leave his survivors with greater than$400,000 in tax-free life insurance policy benefits.< map wp-tag-video: Text boxes appear that read"$400,000 or more of security"and "tax-free revenue through policy car loans and withdrawals"./ wp-end-tag > In reality, throughout every one of the buildup and dispensation years, he'll obtain:$400,000 or even more of protection for his heirsAnd the chance to take tax-free income via policy fundings and withdrawals You're probably asking yourself: How is this feasible? And the solution is basic. Passion is connected to the performance of an index in the supply market, like the S&P 500. But the cash is not straight purchased the securities market. Rate of interest is credited on a yearly point-to-point segments. It can offer you extra control, adaptability, and options for your economic future. Like lots of people today, you may have accessibility to a 401(k) or other retired life plan. And that's a great initial step in the direction of saving for your future. Nevertheless, it's important to comprehend there are restrictions with certified plans, like 401(k)s.

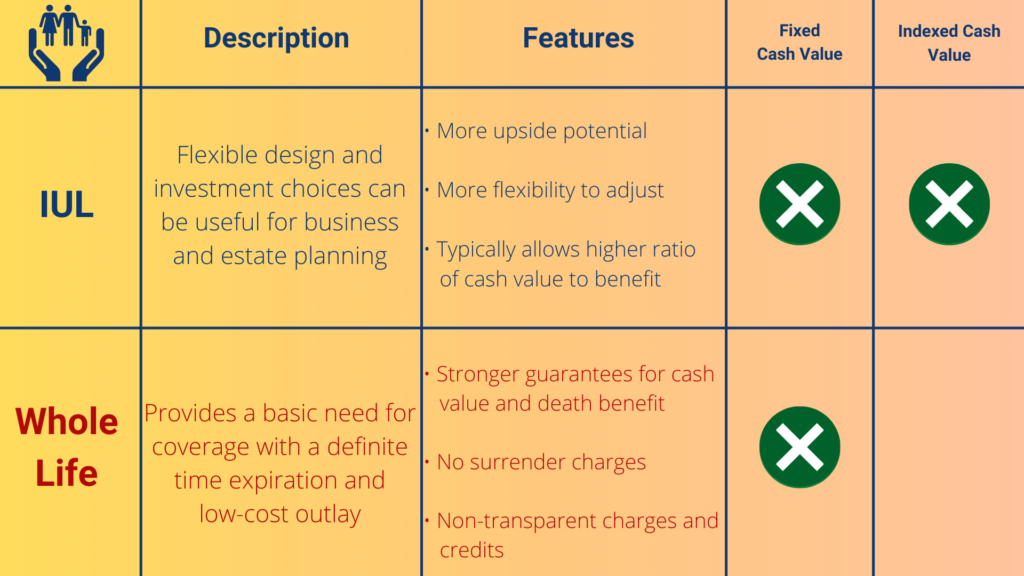

Index Universal Life Insurance Vs Whole Life

And there are limitations on when you can access your cash without charges. [video: Text boxes appear that read "limits on contributions", "restrictions when accessing money", and "money can be taxable".] And when you do take money out of a certified strategy, the money can be taxable to you as earnings. There's an excellent factor many people are turning to this unique remedy to resolve their monetary goals. And you owe it to yourself to see how this can help your own individual scenario. As component of a sound financial strategy, an indexed universal life insurance policy plan can help

Eiul Life Insurance

you handle whatever the future brings. And it supplies distinct possibility for you to build substantial cash money value you can utilize as extra revenue when you retire. Your cash can expand tax delayed with the years. And when the plan is designed properly, distributions and the survivor benefit won't be exhausted. [video: Text box appears that reads "contact your United of Omaha Life Insurance company agent/producer today".] It is very important to seek advice from a specialist agent/producer that comprehends exactly how to structure a remedy such as this correctly. Prior to dedicating to indexed global life insurance, here are some benefits and drawbacks to take into consideration. If you select a good indexed universal life insurance policy strategy, you may see your cash money value grow in worth. This is useful because you might have the ability to gain access to this money before the strategy ends.

Index Universal Life Insurance Fidelity

If you can access it beforehand, it may be helpful to factor it into your. Because indexed global life insurance coverage requires a specific level of risk, insurance provider often tend to keep 6. This type of strategy likewise uses (universal life policy calculator). It is still guaranteed, and you can adjust the face quantity and bikers over time7.

Finally, if the chosen index doesn't do well, your cash money value's development will be impacted. Typically, the insurer has a vested interest in performing much better than the index11. Nevertheless, there is typically an assured minimum rates of interest, so your strategy's growth won't fall listed below a specific percentage12. These are all aspects to be considered when selecting the very best type of life insurance for you.

Buy Iul

Nonetheless, considering that this kind of plan is more complex and has an investment element, it can often feature higher costs than various other plans like whole life or term life insurance policy. If you do not assume indexed global life insurance is appropriate for you, below are some alternatives to consider: Term life insurance policy is a short-lived policy that generally provides insurance coverage for 10 to 30 years.

Indexed universal life insurance policy is a type of policy that supplies a lot more control and adaptability, along with higher cash money value growth possibility. While we do not use indexed global life insurance coverage, we can give you with more info concerning whole and term life insurance policy policies. We advise checking out all your choices and talking with an Aflac representative to find the best fit for you and your household.

The rest is contributed to the money value of the plan after fees are subtracted. The money worth is attributed on a month-to-month or annual basis with rate of interest based on increases in an equity index. While IUL insurance might show beneficial to some, it is very important to comprehend how it functions before buying a plan.

{kind=link}

Latest Posts

Universal Life Insurance With Living Benefits

Best Indexed Universal Life Insurance Companies

Is An Iul A Good Investment